Bitmain’s revenge, Hong Kong’s crypto rollercoaster: Asia Express

Our weekly roundup of news from East Asia curates the industry’s most important developments.

Bitmain allegedly fired staff after salary complaints

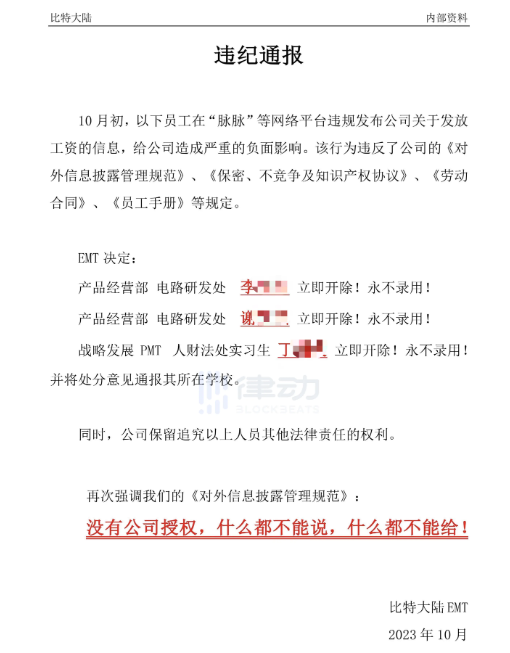

Bitcoin application-specific integrated circuit (ASIC) mining manufacturer Bitmain has allegedly fired three of its employees for speaking to the media regarding the withholding of salary payments by their employer.

According to local news reports on Oct. 17, citing an alleged internal Bitmain memo, the company accused three staff members of breaching various clauses in their employment contracts for sharing their remuneration on social media platforms. The note reads:

“The EMT [Executive Management Team] has decided: (1) Employee Li of product operations and circuit development, is to be fired immediately and blacklisted. (2) Employee Xie of product operations and circuit development, is to be fired immediately and blacklisted. (3) Employee Ding, administrative intern at strategic development PMT, is to be fired immediately and blacklisted. The intern’s post-secondary institution shall also be informed of the incident.”

“In addition, the company reserves the right to pursue legal action against the individuals above,” Bitmain allegedly wrote. “Without authorization by the company, nothing can be said, nothing can be given [to outsiders!]”

On Oct. 9, Cointelegraph reported that Bitmain allegedly paused September salary payments for its staff members as the company “has yet to achieve a net positive cash flow, especially in the orders of [new] ASICs.” In addition, employees allegedly face a 50% cut to their base salary, with all bonuses and incentives being removed.

Founded in Beijing, China in 2013, Bitmain is one of the world’s largest Bitcoin mining ASIC manufacturers, with an estimated 70% market share during the previous bull market that ended in 2021. The firm’s Antminer ASIC series currently leads the industry in terms of hash rate computations for mining Bitcoin. Over the past year, several Bitcoin mining operators have gone bankrupt as the price of Bitcoin plunged while electricity costs surged.

Hong Kong investors spooked by JPEX scandal

Despite efforts to regulate the sector, it appears that some Hong Kong residents have lost their confidence in crypto after the largest Ponzi scheme in the city’s history, the $175 million JPEX crypto exchange scandal, unfolded last month.

According to a new study published by the HKUST Business School Central on Oct. 17, 41% of Hong Kong residents are no longer interested in holding crypto assets, a sharp rise of 12% compared to before the JPEX incident. The survey featured 7,900 respondents and was conducted between April and October.

The study also revealed that 84% of Hong Kongers have heard of crypto, with 27% of respondents claiming they either hold digital assets now or were previously crypto investors. For those investing in crypto, over 80% said they would not invest over 50,000 Hong Kong dollars ($6,390) into the sector. Interestingly, 57% of respondents said they understood that crypto exchanges must obtain a license before operating in Hong Kong, an increase of 15% compared to before the JPEX scandal unraveled.

Wu Huang, a professor at HKUST Business School Central, commented:

“We hope that the results of this survey can provide industry stakeholders with more perspectives to help build a sound virtual asset industry. As virtual assets play an increasingly important role in the digital economy, there is a need to strengthen education efforts to make the public better Understand the risks and potential of this emerging field.”

Last month, JPEX staff fled their corporate booth at Singapore’s Token2049 event after the Hong Kong Securities and Futures Commission issued a warning regarding the exchange’s unregulated activities. Subsequently, Hong Kong police arrested more than 10 corporate executives and influencers connected to the exchange on charges of fraud. The JPEX scandal has since grown to over 2,300 victims, with losses estimated at $175 million. The exchange was unlicensed at the time of the incident.

Read also

“Factually inaccurate” news report wipes out $54 million in market cap

When it comes to reporting, Cointelegraph has seen some blunders over the years. That said, fake news is a problem across the industry.

On Oct. 16, Bloomberg reported that BC Technology Group, owner of licensed Hong Kong crypto exchange OSL, is contemplating the sale of the latter for 1 billion Hong Kong dollars ($128 million).

On Oct. 17, BC Technology Group issued a clarification stating: “The Board wishes to clarify that the contents and statements in the [Bloomberg] Article are factually inaccurate and highly misleading” and that it was not contemplating a sale of OSL.

Unfortunately, investors who bought BC Technology stock based on the divestiture euphoria were not so happy. After publishing the clarification statement, shares of BC Technology tanked 22% during the trading day, wiping off $54 million in market capitalization. “Shareholders of the Company and potential investors are advised to exercise caution when dealing in the shares of the Company,” management wrote.

Bitget’s new crypto credit card

Joining the likes of its peers, cryptocurrency exchange Bitget is launching its own crypto-fiat credit card. According to an Oct. 16 announcement during the Future Blockchain Summit in Dubai, the Bitget Card, issued by Visa and backed by digital assets in users’ accounts and wallets, will be denominated in U.S. dollars and will be accepted in over 180 countries.

Although many exchanges have rolled out their own crypto debit or credit cards, some have seen pushback from payment processors. On Aug. 25, Mastercard said it would end its cryptocurrency card partnership with Binance in Latin America. Although the firm did not cite a specific reason, experts have pointed to Binance’s recent regulatory scrutiny as the underlying cause.

Subscribe

The most engaging reads in blockchain. Delivered once a week.