Hallelujah

(Any views expressed here are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

Want More? Follow the Author on Instagram, LinkedIn and X

Access the Korean language version here: Naver

Subscribe to see the latest Events: Calendar

Praise be to Lord Satoshi that time and compounding interest exist regardless of who you are.

Even if you are a government, there are only two ways to pay for stuff, using savings or debt. For a government, savings equates to taxes. Taxes are not very popular, but spending is. Therefore, when handing out goodies to the plebes and patricians, politicians prefer to issue debt. Politicians will always favor borrowing from the future to get re-elected in the present, because when the bill comes due, they won’t be in office.

If all governments, because of the incentives of its officers, are hard wired to prefer issuing debt rather than raising taxes to hand out goodies, then the next question is how do buyers of government debt fund these purchases? Do they spend their savings/equity or finance purchases by borrowing money?

Answering these questions as it pertains to Pax Americana is very important to my forward outlook of dollar money creation. If the marginal buyer of US treasury debt finances their purchases, then we can observe who is lending to them. Once we know the identities of the debt financiers, we can determine whether they create money ex nihilo or use their own equity to lend. If after answering all the questions we discover that a treasury financier creates money for lending then we can market the following leap of logic.

Government issued debt grows the money supply.

And if this statement is true, then we estimate the maximum amount of credit that the financier can issue, assuming there is a maximum.

The reason these questions are important is that I will argue that if government borrowing continues as forecast by the Too Big to Fail (TBTF) Banks, the US Treasury Department, and the Congressional Budget Office, then the Fed’s balance sheet will grow as well. If the Fed’s balance sheet grows, that is dollar liquidity positive, and ultimately pumps the price of Bitcoin and other cryptos.

Let’s step through the questions and evaluate this logic puzzle.

Question Time

Will US President Trump cut taxes to fund the deficit?

No. He and the Team Red Republicans recently extended the 2017 tax cuts.

Is the Treasury Department borrowing money to fund the federal deficit, and will they continue to do this in the future?

Yes.

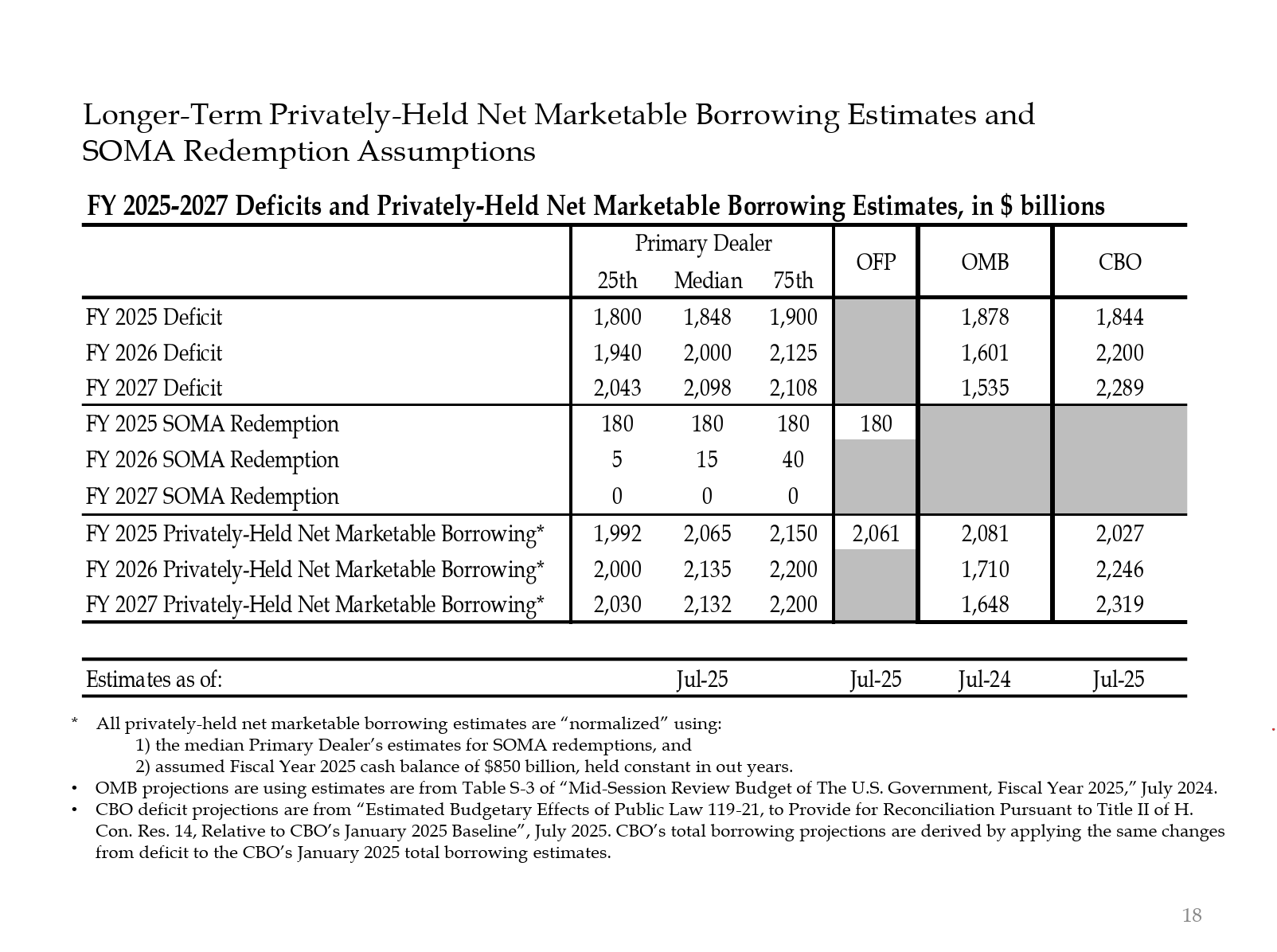

Here are the estimates from the TBTF banksters, and a few US government agencies. As you can see, the estimates are for ~$2 trillion deficits funded by ~$2 trillion of borrowing.

Given the answer to the first two questions is Yes, then:

Yearly Federal Deficit = Yearly Treasury Debt Issuance Amount

Let’s step through the major buyers of treasuries and how they finance their purchases.

Debt Shit Eaters

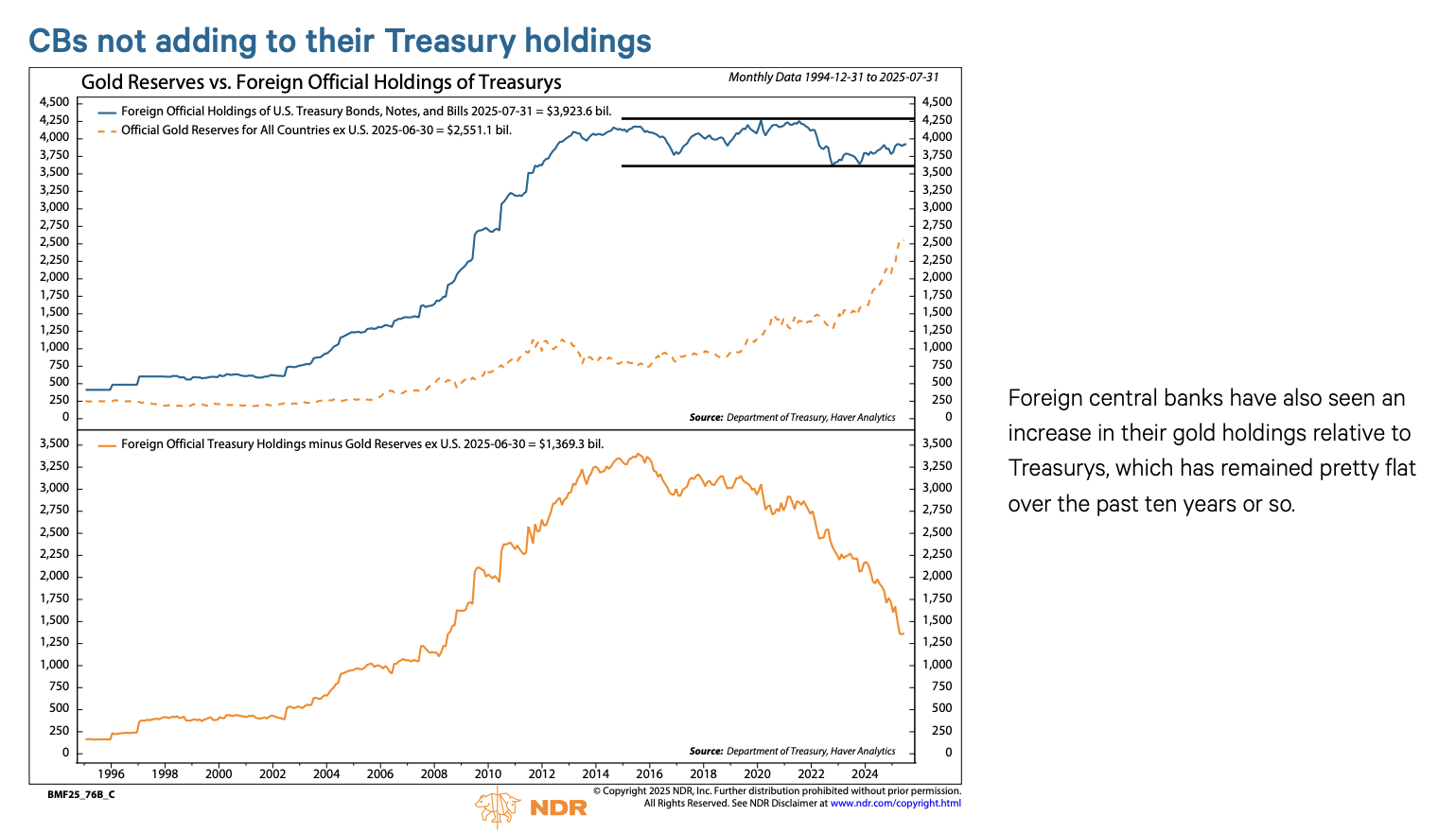

Foreign Central Banks

If Pax Americana is willing to steal Russia’s money, who is a nuclear power and the largest commodity exporter in the world, then no foreign owner of treasuries is ever safe. Cognizant of the risk of expropriation, foreign central bank reserve managers would rather buy gold than treasuries. Therefore, gold started ripping for realz post Russia’s invasion of Ukraine in February 2022.

US Private Sector

According to the US Bureau of Labor and Statistics, the 2024 personal savings rate was 4.6%. In the same year, the US federal deficit was 6% of GDP. Given that the deficit is larger than the savings rate, it is impossible for the private sector to be the marginal buyer of treasuries.

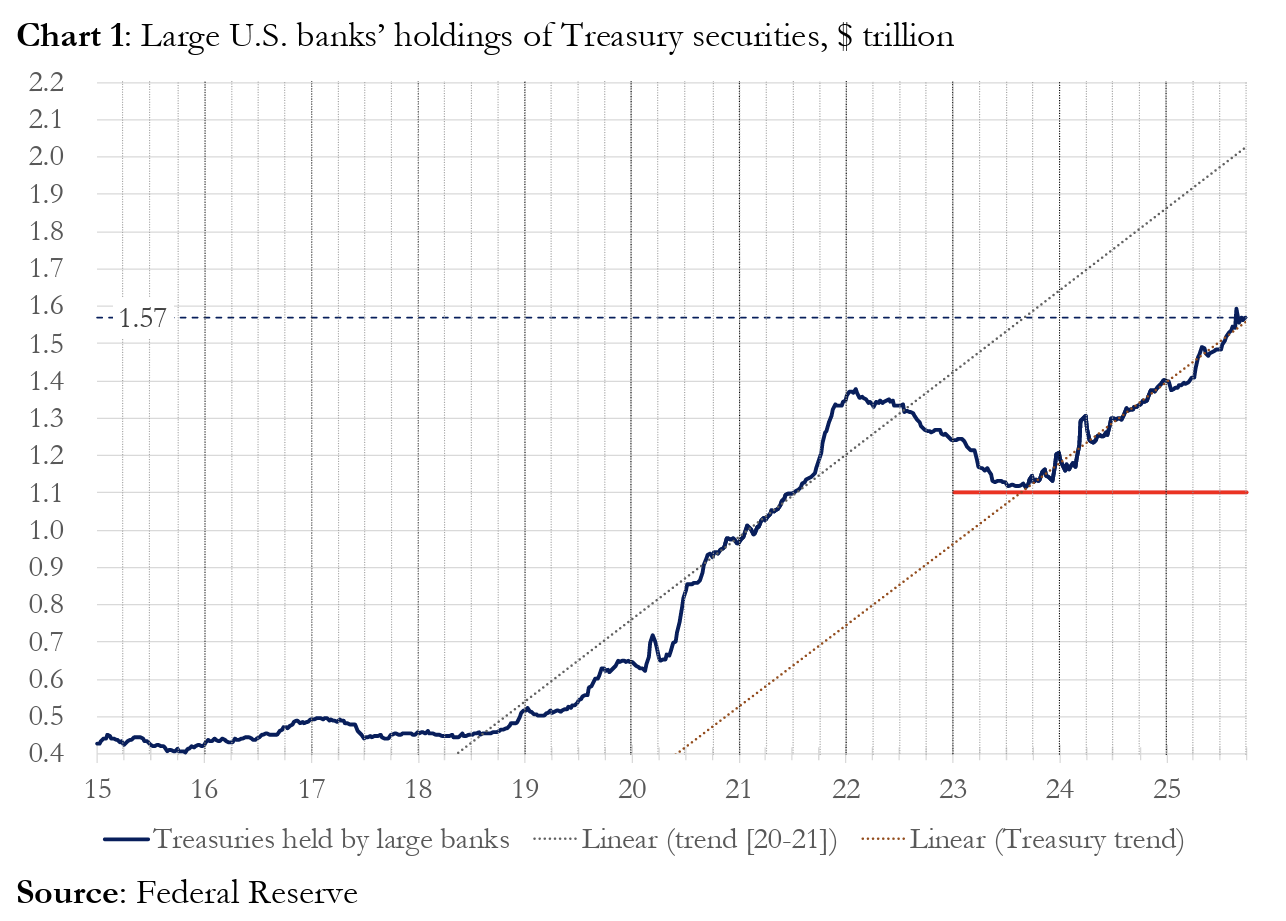

Commercial Banks

Are the four largest money center commercial banks buying shit loads of treasuries? No.

As you can see the four large money center banks in the fiscal year 2025 bought ~$300 billion worth of treasuries. In the same fiscal year, the treasury issued $1,992 billion. While this cohort is definitely an important buyer of treasuries, they are not the marginal buyer of last resort.

Relative Value (RV) Hedge Funds

RV funds are the marginal buyers of treasuries as acknowledged by the Fed in a recent paper.

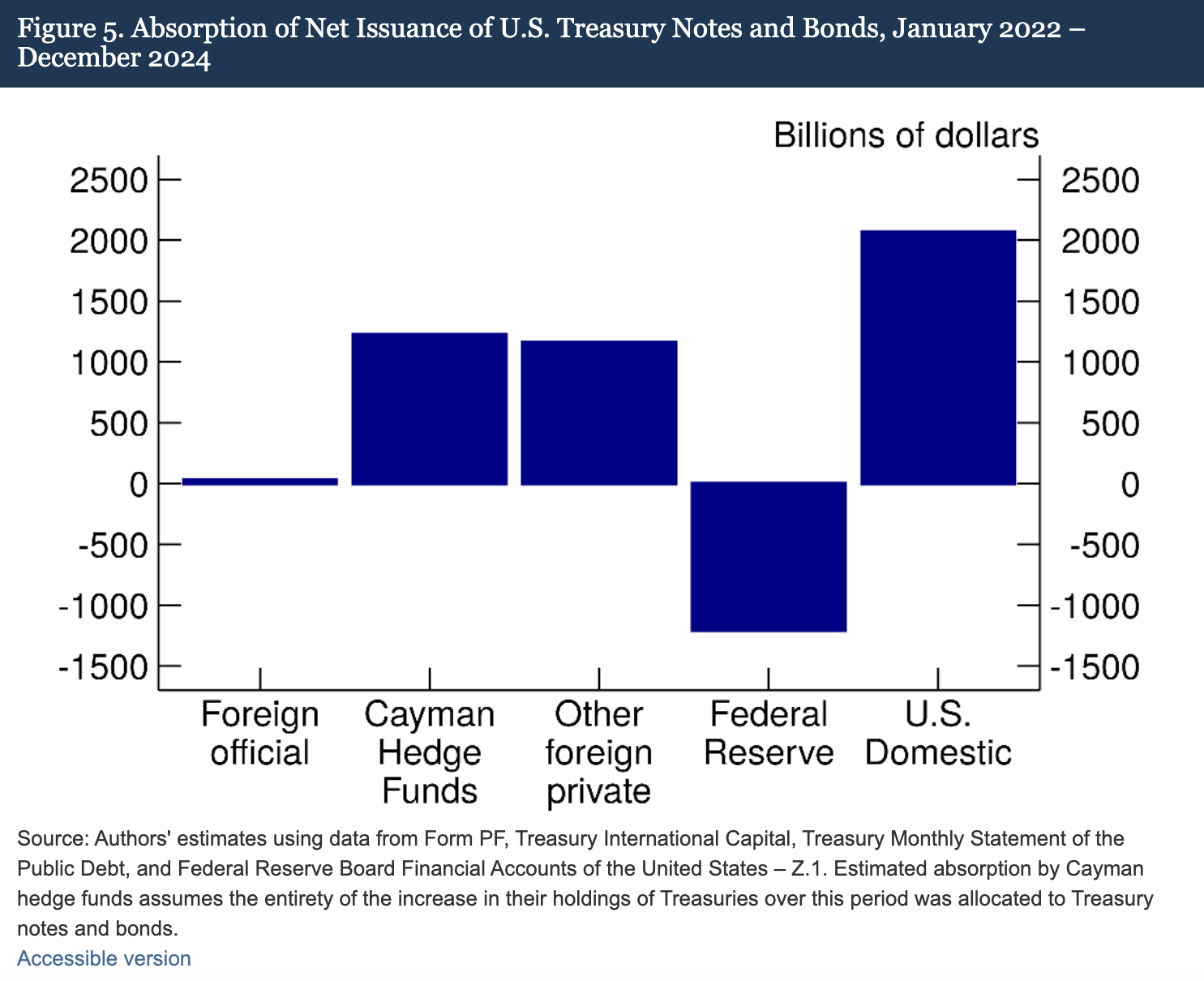

Our findings suggest that Cayman Islands hedge funds are, increasingly, the marginal foreign buyers of U.S. Treasury notes and bonds. As shown in Figure 5, between January 2022 and December 2024, a time when the Federal Reserve was reducing the size of its balance sheet by allowing maturing Treasuries to roll off from its portfolio, Cayman Islands hedge funds purchased, on net, $1.2 trillion of Treasury securities. Under the assumption that these purchases are composed entirely of Treasury notes and bonds, they absorbed 37% of net issuance of notes and bonds, nearly the same amount as all other foreign investors combined.

The Trade:

Buy a cash treasury debt security

Vs.

Sell the corresponding treasury futures contract

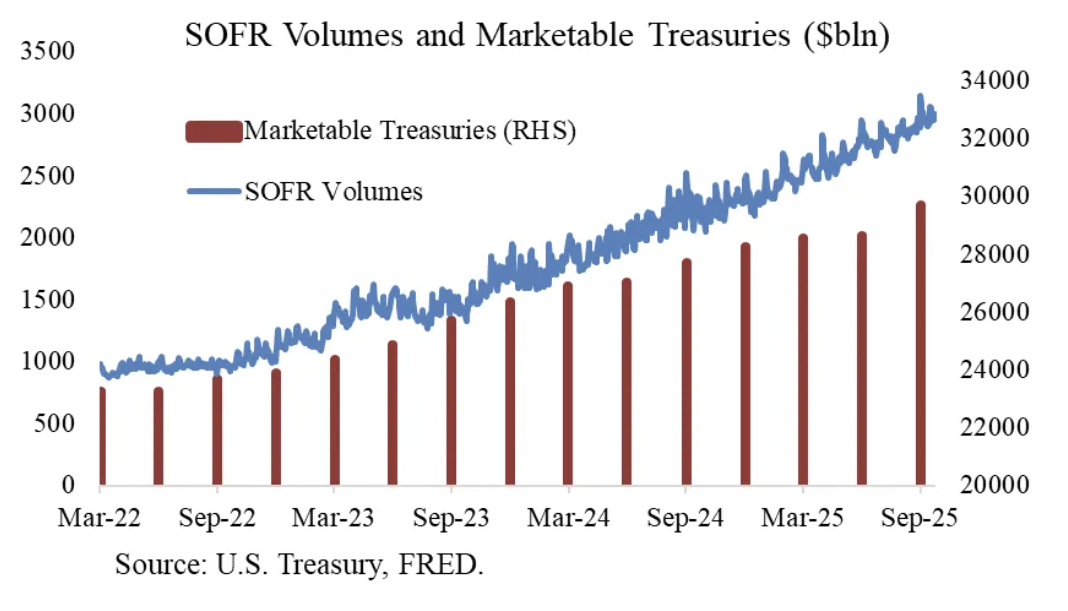

Thank you, Joseph Wang for this chart. SOFR volumes are a proxy for gauging the size of the RV funds’ participation in the treasury markets. As you can see, the growth in the debt load corresponds to a growth in SOFR volumes. This shows that RV funds are the marginal buyers of treasuries.

RV funds conduct this trade to earn the difference between the two instruments. Because the spread is miniscule (it’s measured in basis points; 1bps = 0.01%), the only way to make real money is to finance the purchase of the treasury security. This leads us to the most important part of this essay to understand what the Fed will do next. How do RV funds finance their treasury purchases?

RV funds engage in a repurchase agreement (repo) to finance the purchase of treasuries. In a seamless transaction, the RV fund pledges the treasury security it purchased to borrow overnight cash, that borrowed cash is then used to settle the treasury purchase. If cash is plentiful, the repo rate will trade at or right below the Upper Fed Funds. Why?

Let’s revisit how the Fed manipulates short term interest rates. The Fed has two policy rates, Upper and Lower Fed Funds; currently these equal 4.00% and 3.75% respectively. In order to force the effective short-term rate (the SOFR or Secured Overnight Funding Rate) to fall within that band, the Fed uses a few blunt instruments. I will go through them briefly, ordered from lowest to highest rate of interest.

Reverse Repo Facility (RRP)

Who is eligible: Money market funds (MMF) and commercial banks

Purpose: Cash deposited here overnight earns a rate of interest paid for by the Fed.

Award Rate: Lower Fed Funds

Interest on Reserve Balances (IORB)

Who is eligible: Commercial banks

Purpose: Banks receive interest on their excess reserves deposited at the Fed.

Award Rate: Between Lower and Upper Fed Funds

Standing Repo Facility (SRF)

Who is eligible: Commercial banks and other financial institutions

Purpose: When cash is tight, this allows financial institutions pledge eligible securities (mostly treasuries) and receive cash from the Fed. In effect, the Fed prints money and exchanges it for the pledged security.

Award Rate: Upper Fed Funds

Putting it all together we get this relationship:

Lower Fed Funds = RRP < IORB < SRF = Upper Fed Funds

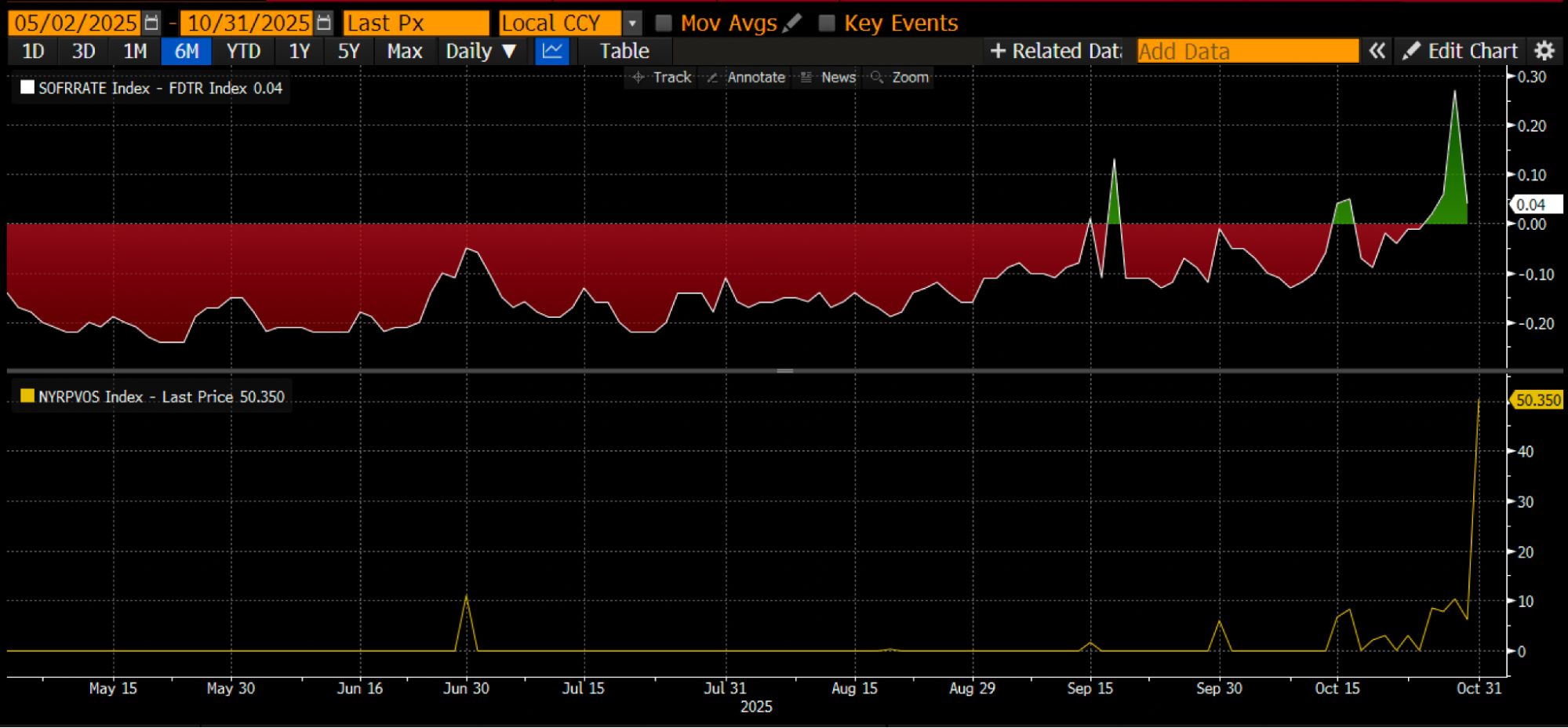

This is a useful chart of real-world values to visualize the relationship between these key USD money market rates. At the top the orange (SRF) and green (Upper Fed Funds) are equal. Right below that we have the red line (IORB). The magenta line (SOFR) usually vacillates between the upper and lower bound. The yellow (Lower Fed Funds) and white (RRP) are equal.

SOFR is a blend of the rate on multiple types of repo transactions. Unlike the London Interbank Offered Rate (LIBOR) which was based on bank submissions, SOFR is based on actual market trades. This is the rate the Fed targets. If SOFR trades above the Upper Fed Funds it means cash is tight and this is a problem. Because once cash gets tight, SOFR skyrockets and the filthy fiat financial system shuts down. That is because the marginal buyers and suppliers of liquidity are all levered. If they cannot roll over their liabilities predictably at Fed Funds, then they will first suffer massive losses, and subsequently cease providing liquidity to the system. The worry is that no one will participate in the treasury market because they cannot obtain cheap leverage.

What causes SOFR to trade above the Upper Fed Funds? To answer that question, we first must inquire who is the marginal provider of cash in the repo market? MMFs and commercial banks supply the repo market with cash. Let’s examine why they would do so assuming they are profit maximizing entities.

The goal of an MMF is to take as little credit risk as possible and earn the short-term interest rate. This means MMFs mostly earn a return parking money in the RRP, lending cash in the repo market, and buying treasury bills (T-bills). In all three cases they take the credit risk of the Fed or the US Treasury, which is essentially risk free because the government can always print money to service its debts. Prior to the emptying of the RRP, the billions or trillions of dollars sat there would supply the repo market with cash. That is because RRP < SOFR, so a profit maximizing MMF will remove cash from the RRP and lend it in the repo market. But now the RRP balance is zero because the T-bill rate is so attractive; MMFs maximize profit by lending to the US government.

With the MMFs out of the game, commercial banks must fill the gap. They will happily lend reserves to the repo market because IORB < SOFR. The gating factor to how willing banks are to supply cash at “reasonable” levels, that is SOFR <= Upper Bound of Fed Funds, depends on how ample their reserves are. There are various regulatory requirements that force banks to keep a certain amount of reserves, once balance sheet capacity dwindles, they must charge higher and higher rates to supply cash to the repo markets. Banks lost trillions in reserves since the Fed began QT in early 2022.

Both marginal providers of cash, MMFs and banks, from 2022 onwards possess less cash with which to supply the repo market. At a certain point, neither was willing nor able to provide cash in the repo market at a rate at or below Upper Fed Funds. At the same time as the supply of cash that could supply the repo market at a reasonable rate fell, the demand for said cash rose. The demand rose because former US President Biden and now Trump continued to spend a fuck ton of money that required more treasury debt issuance. The marginal buyer of this debt, RV funds, must finance these purchases in the repo market. If they cannot predictably obtain funds daily at or slightly below Upper Fed Funds, they will not buy treasuries and the US government cannot finance itself at an affordable rate. For a more in-depth discussion of this please read my essay “Ski Cut”.

Because a similar situation occurred in 2019, the Fed created the SRF. The Fed can supply an infinite amount of cash using its printing press at SRF as long as one provides an acceptable form of collateral. Therefore, RV funds can be confident that no matter how tight cash is, they can always fund themselves, in the worst case, at Upper Fed Funds.

If the SRF balances are above zero, then we know the Fed is cashing the checks of the politicians using printed money.

Treasury Debt Amount Issued = Increase in Supply of Dollars

The top panel is (SOFR – Upper Fed Funds). When that difference is close to zero or positive, cash is tight. During these episodes non-trivial usage of the SRF (bottom panel, in USD billions) occurs. Usage of the SRF allows borrowers to avoid paying the higher less manipulated SOFR rate.

Stealth QE

There are two ways the Fed can ensure that there is ample cash in the system to facilitate the repos needed by RV funds to purchase dog shit treasuries. The first is to create banking reserves, by buying securities from banks. This is the textbook definition of QE. The second is to lend freely to the repo market via the SRF.

As I have said many times, QE is a dirty word. Even the most financially illiterate plebe now understands QE = money printing = inflation. When inflation bites, the average citizen votes for the opposition party. Given that Trump and Buffalo Bill Bessent want to run the economy hot, they don’t want to be blamed for the high inflation a credit fueled economic expansion will generate. Therefore, the Fed will do everything it can, with a straight face, to proclaim that its policy mix is not QE and does not stoke the fires of inflation. Ultimately, that means that the SRF is the conduit through which printed money enters the global financial system as opposed to using QE to create more banking reserves.

This will buy some time, but eventually the exponential expansion of treasury debt issuance will force the repeated use of the SRF. Remember that not only does Buffalo Bill Bessent need to issue $2 trillion annually to fund the government, he also must issue trillions more to roll over maturing debt. Stealth QE will begin shortly. I don’t know when it will begin. But if the current money market conditions persist, the treasury debt pile grows exponentially, the SRF balance must grow as the lender of last resort. As SRF balances grow, the amount of fiat dollars in the world expands as well. This phenomenon will reignite the Bitcoin bull market.

Between now and when stealth QE begins, one has to husband capital. Expect a choppy market especially until the US government shutdown ends. The treasury via its debt auctions is borrowing money (dollar liquidity negative) but not spending it (dollar liquidity positive). The Treasury General Account is above the $850 billion target by ~$150bn, and this extra liquidity won’t get released into the markets until the government reopens. This liquidity drain is one reason for the current softness in the crypto markets. Given that the four-year cycle anniversary of the 2021 Bitcoin all-time-high is nigh, many will mistake this period of market weakness and ennui as the top and dump their stack. That’s assuming they weren’t deaded in the altcoin collapse a few weeks back. That is a mistake, the dollar money market plumbing doesn’t lie. This corner of the market is shrouded in obtuse jargon, but once you translate the lingo into print money or destroy money, it becomes quite easy to know how to dance.

Want More? Follow the Author on Instagram, LinkedIn and X

Access the Korean language version here: Naver

Subscribe to see the latest Events: Calendar

The post Hallelujah appeared first on BitMEX Blog.

BitMEX Blog