Central banks will face unfamiliar challenges to achieve CBDC inclusivity, study says

A common argument made in favor of central bank digital currency (CBDC) is that it could boost financial inclusion. The nuances of how to accomplish that goal, or even what “financial inclusion” means, remain to be explored, a Bank of Canada discussion paper said. It concluded that central banks will face a range of unfamiliar and nontraditional challenges to create an inclusive CBDC.

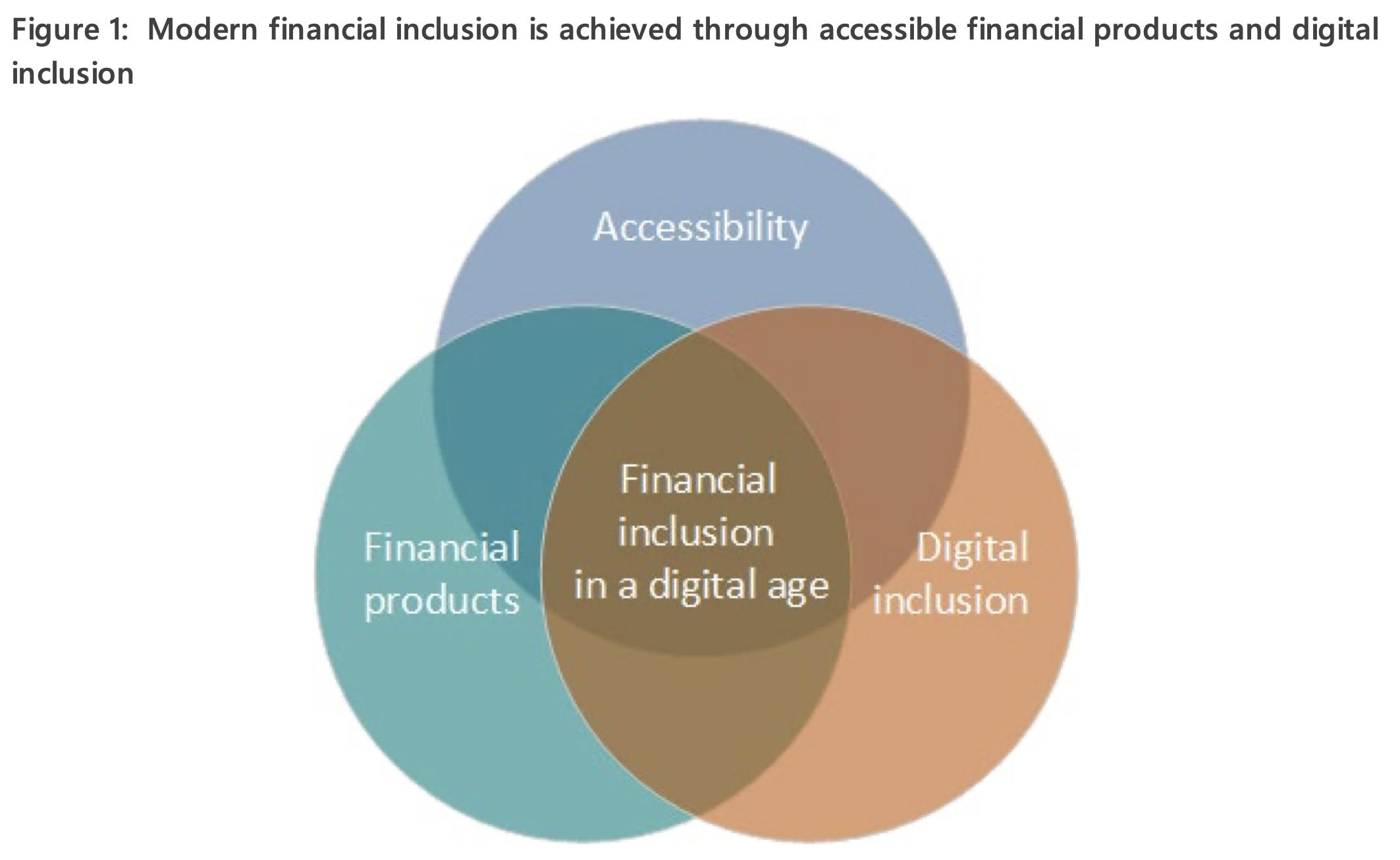

By “identifying material barriers and describing the realities of inequity underlying the aggregate statistics that are commonly used” the authors of the paper identified three types of inclusion necessary for a universally accessible payment method: financial inclusion, digital inclusion and practical accessibility. Private financial institutions may not have an incentive to address the needs of those who are underserved. In this light, the authors said:

“Our analysis suggests that the number of individuals who face barriers or exclusion is much larger than was previously assumed.”

Unless all three aspects of accessibility are accounted for, persons who experience challenges in one type of inclusion may have the same disadvantages if a CBDC is introduced, the authors state. For example, members of the First Nations on average live at a much greater distance from financial institutions than other Canadians (25 km. vs. 1.9 km.) and their financial inclusion would depend on digital inclusion.

Financial literacy and ease of use come into play as well. First Nations youth are likely to have digital access but be less skilled in the use of digital technology than their non-Indigenous peers, the authors say. Other Canadians may be hesitant to use digital technology due to exaggerated fears about security.

On #NTRD, show your support by taking part in your local activities.

Start your learning journey:

https://t.co/OP0c25sx8N

#TruthandReconciliation #OrangeShirtDay pic.twitter.com/rja20HuaS1— Bank of Canada (@bankofcanada) September 30, 2023

Cognitive load – the level of difficulty in using digital financial technology – and other usability issues are potential barriers to accessibility that are likely to grow as the population ages. Older people use smartphones less than younger and less than 60% of the population was assessed as having internet skills that could be rated proficient or advanced, according to a survey cited. The problem requires “deeper research into design for cognitive accessibility,” the authors said.

Related: Insurance, agriculture, real estate: How asset tokenization is reshaping the status quo

Disabled people may experience greater difficulty in using the technology as well. Disabled people in Canada have considerably less access to the internet than other Canadians.

The challenge is in the delivery of services, rather than the nature of CBDC itself, the authors stated. Overcoming those challenges will require central banks to face problems that would otherwise be considered far from their scope of interest.

The study looked at the needs of specific segments of the Canadian population. A previous study found that the majority of Canadians have little reason to use a CBDC because of the high level of accessibility of financial services in the country.

Magazine: Should you ‘orange pill’ children? The case for Bitcoin kids books